what do balance sheets show and the tie back to k-1s

Residual Sheet Reconciliation is the reconciliation of the closing balances of all the accounts of the visitor that forms office of the company'south residual canvass in order to ensure that the entries passed to derive the closing balances are recorded and classified properly so that balances in the residual canvas are appropriate.

What is a Balance Sail Reconciliation?

Reconciliation of balance sheet merely means the reconciliation Companies practise reconciliation prior to endmost their books of accounts to match balances in different accounts and to business relationship for the double result of periodical entries. It assists in ensuring that the books are upward to date and that in that location is no manipulation, fraud, missing, or wrong entries in the firm'south books of accounts. read more than of closing balances of all transactional and ledger entries and accounts. Information technology forms office of the balance sheet items Assets such as cash, inventories, accounts receivable, investments, prepaid expenses, and fixed avails; liabilities such as long-term debt, short-term debt, Accounts payable, and so on are all included in the balance sheet. read more than for a respective financial twelvemonth and whether it is being recorded and properly classified, making up to the balances appropriately in the remainder sail. Information technology is a final and crucial activity that the company performs to ensure the accuracy of its financial statements Financial statements are written reports prepared by a company's management to nowadays the company's fiscal affairs over a given menstruum (quarter, six monthly or yearly). These statements, which include the Residuum Sheet, Income Statement, Cash Flows, and Shareholders Equity Statement, must be prepared in accord with prescribed and standardized accounting standards to ensure uniformity in reporting at all levels. read more before the endmost of its books at the terminate of the financial wheel.

You lot are gratuitous to use this image on your website, templates etc, Please provide us with an attribution link Article Link to be Hyperlinked

For eg:

Source: Balance Canvas Reconciliation (wallstreetmojo.com)

Types/Components of Residuum Sheet Reconciliation

There are ii types of formats in which a balance sheet can be prepared. I is the horizontal format or called the T-format, and the other format is the Vertical Format. The contents in both the format are, withal, the aforementioned. It is just the mode it gets presented is dissimilar. Presently the vertical format is widely being in use.

The components of the balance sheet A balance sheet is one of the financial statements of a company that presents the shareholders' equity, liabilities, and assets of the visitor at a specific point in fourth dimension. It is based on the accounting equation that states that the sum of the total liabilities and the owner'due south capital equals the full avails of the visitor. read more contain data, which would either increase or decrease revenue. Hence many of these would have already been computed. In contrast, the preparation on income and expense / Profit and Loss statements, and a few would be carried forward from the previous twelvemonth'south balances shall just have the final balances available in these accounts.

Ideally, a residuum canvass would accept the following components:- "Avails, Liabilities, and Owner'south Equity."

- Assets are items that would probable increase or generate revenue for the company—examples: cash, receivables, inventory, prepaid expenses Prepaid expenses refer to advance payments made by a house whose benefits are acquired in the futurity. Payment for the appurtenances is fabricated in the current bookkeeping period, but the delivery is received in the upcoming accounting menstruation. read more , and fixed assets, etc.

- Liabilities Liability is a financial obligation as a outcome of any by event which is a legal binding. Settling of a liability requires an outflow of an economic resource by and large coin, and these are shown in the residue of the company. read more are items which would probable subtract the revenue for the visitor. Examples: Debts, accounts payable Accounts payable is the amount due by a business to its suppliers or vendors for the purchase of products or services. It is categorized as current liabilities on the balance canvass and must be satisfied inside an bookkeeping period. read more , payroll and taxes payable, notes payable Notes Payable is a promissory note that records the borrower's written hope to the lender for paying up a certain amount, with interest, by a specified date. read more than , deferred revenue Deferred Revenue, also known as Unearned Income, is the advance payment that a Company receives for goods or services that are to be provided in the futurity. The examples include subscription services & accelerate premium received by the Insurance Companies for prepaid Insurance policies etc. read more , and customer deposits, etc.

- At that place is no such formula to summate the residuum canvass every bit it is a statement to match the total liabilities with total assets. However, this tin exist represented in the following form:- Assets + Owners Equity = Liabilities.

Balance Sheet Reconciliation Template

Given Below is the Template of the Balance sail reconciliation.

| Visitor Proper name | |||||

| Balance Sheet as at MM/DD/YYYY | |||||

| Stock-still assets | |||||

| Intangible assets Intangible Assets are the identifiable assets which practise not take a physical existence, i.due east., you can't touch them, like goodwill, patents, copyrights, & franchise etc. They are considered as long-term or long-living assets as the Company utilizes them for over a twelvemonth. read more | 30 | It is the total value of development costs incurred by the business plus the cost of the license it holds for selling its goods. | |||

| Tangible assets Tangible assets are assets with significant value and are available in physical form. It means any asset that tin can be touched and felt could be labeled a tangible one with a long-term valuation. read more | xxx | It is the cost of the business organisation premises, furniture | |||

| and equipment, less depreciation charged since first using the assets | |||||

| Investments | xxx | It is the value of shares owned in DEF Utilities PLC | |||

| xxx | |||||

| Electric current avails | |||||

| Stock | 30 | Information technology is the total value of goods bought from suppliers that have non yet been sold plus raw materials held for product plus the value of piece of work in progress. | |||

| Debtors | |||||

| Trade debtors | 30 | Information technology is the full of the amounts customers owe, less bad debts Bad Debts can be described every bit unforeseen loss incurred by a business system on account of non-fulfillment of agreed terms and atmospheric condition on account of sale of goods or services or repayment of whatever loan or other obligation. read more and amounts considered uncollectable | |||

| Prepayments and accrued income Accrued Income is that office of the income which is earned but hasn't been received nevertheless. This income is shown in the balance sheet equally accounts receivables. read more | xxx | It is the maintenance fee payable annually in advance to the computer software visitor. | |||

| xxx | |||||

| Cash at bank and in paw | xxx | It is the total of cash kept on site and the balance on the business' current account with the depository financial institution. | |||

| xxx | |||||

| Creditors: amounts falling due within One Year | Also known as current liabilities Current Liabilities are the payables which are likely to settled within twelve months of reporting. They're usually salaries payable, expense payable, brusque term loans etc. read more than – liabilities are shown as negatives because they are amounts owed by the business. | ||||

| Bank loans and overdrafts | thirty | Information technology is the portion of the business' bank loan, which is due to be repaid in the next twelve months. | |||

| Merchandise creditors | 30 | It is the total of the amounts owed by the business organization to its suppliers for goods it bought to sell to its customers. | |||

| Other creditors including taxation and social security | 30 | It is the value of tax and national insurance contributions deducted from employee salaries that accept non even so been paid over to the Inland Acquirement. | |||

| Accruals and deferred income Deferred Acquirement, too known every bit Unearned Income, is the advance payment that a Company receives for appurtenances or services that are to be provided in the time to come. The examples include subscription services & advance premium received by the Insurance Companies for prepaid Insurance policies etc. read more | xxx | It includes interest due to the depository financial institution loan since the last repayment. | |||

| 30 | |||||

| Net current avails | xxx | Likewise known as working uppercase Working majuscule is the amount bachelor to a company for day-to-24-hour interval expenses. It's a measure of a company'due south liquidity, efficiency, and fiscal health, and it's calculated using a simple formula: "electric current assets (accounts receivables, greenbacks, inventories of unfinished appurtenances and raw materials) MINUS electric current liabilities (accounts payable, debt due in ane year)" read more – this shows the business' power to meet electric current obligations. | |||

| Total assets less current liabilities | 30 | ||||

| Creditors: amounts falling due after more than 1 year | |||||

| Banking concern loan | xxx | It is the portion of the business organization' bank loan, which is due to be repaid in over one year. | |||

| Cyberspace assets | xxx | ||||

| Capital and reserves | |||||

| Called upwards share capital Share capital refers to the funds raised by an organization by issuing the visitor'due south initial public offerings, mutual shares or preference stocks to the public. Information technology appears as the possessor'south or shareholders' equity on the corporate residue canvass's liability side. read more than | xxx | These are the funds invested by the owners in the concern, east.one thousand., to finance its assets. | |||

| Profit and loss account The Turn a profit & Loss business relationship, also known as the Income statement, is a financial statement that summarizes an organization's revenue and costs incurred during the financial period and is indicative of the company's financial performance by showing whether the company made a profit or incurred losses during that menstruum. read more than | 30 | These are the profits made since the start of the business concern, fewer expenses, and amounts paid to the owners as dividends Dividends refer to the portion of business earnings paid to the shareholders as gratitude for investing in the visitor'south disinterestedness. read more . | |||

| Shareholders' funds | xxx |

Examples of Balance Sheet Reconciliation

Now, let's come across some examples of the Rest sheet reconciliation.

Balance Sheet Reconciliation Example #1

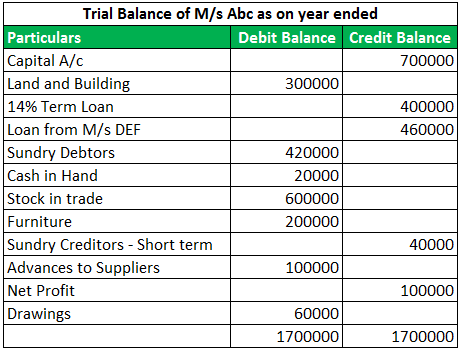

Following is the trial balance Trial Residue is the report of accounting in which ending balances of a different general ledger are presented into the debit/credit column as per their balances where debit amounts are listed on the debit cavalcade, and credit amounts are listed on the credit column. The total of both should be equal. read more than of M/Due south ABC at the stop of the yr. Ready a balance canvass for the same.

Solution:

Beneath is the reconciliation of the Residuum Sheet.

We note hither that the total net assets are equal to total net liabilities (740,000)

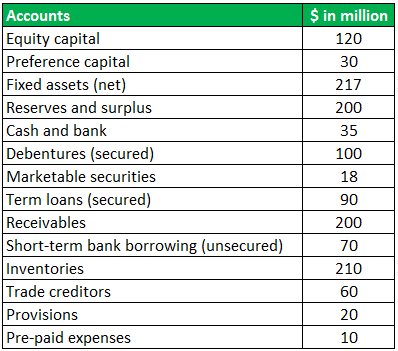

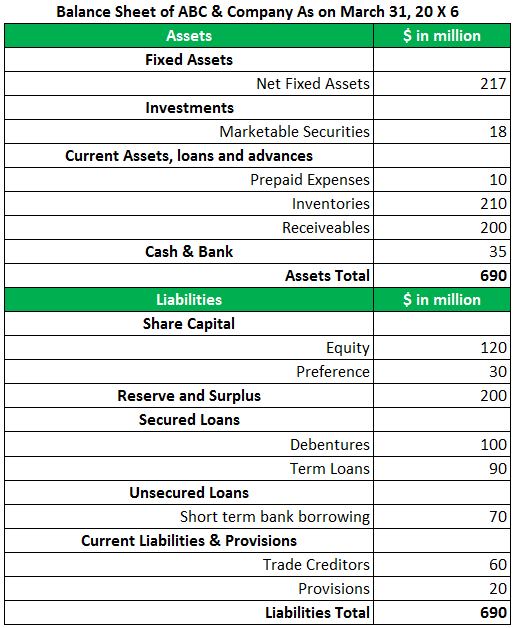

Residuum Sheet Reconciliation Example #2

At the end of March, 20X6 the balances in the diverse accounts of ABC & Company are as follows:

Fix the balance canvass of ABC & Company as per the format.

Solution:

Below is the rest sheet reconciliation.

Once more, nosotros encounter that the full avails are equal to total liabilities.

Advantages

Reconciling of remainder sheet shall provide many and multiple benefits. However, a few of the fundamental and main benefits are:

- Eliminates bookkeeping errors Accounting errors refer to the typical mistakes made unintentionally while recording and posting accounting entries. These mistakes should not be considered fraudulent behaviour first-hand every bit this tin can happen with anyone and by anyone. read more

- To better empathize and evaluate the fiscal strength of the visitor

Disadvantages

Manual reconciliation of balance sheets or whatever accounts is prone to take errors due to the manual intervention involved. Hence it involves a risk of information manipulation, missing the recording of data, etc.

Recommended Articles

It has been a guide Balance Canvass Reconciliation. Hither we talk over how to reconcile the Residuum canvas using endmost balances, ledger entries, and bookkeeping transactions along with practical examples. You can learn more about accounting from the post-obit articles –

- Balance Sheet Ratios

- How to Read a Balance Sheet?

- Examples of Balance Canvass

- Equation of Residue Sheet

- one Online Courses

- 3+ Hours

- Verifiable Certificate of Completion

- Lifetime Admission

Learn MORE >>

brindletherage1977.blogspot.com

Source: https://www.wallstreetmojo.com/balance-sheet-reconciliation/

{kind=link}

Post a Comment for "what do balance sheets show and the tie back to k-1s"